US indices finished yesterday’s session higher. S&P 500 jumped 0.48%, Nasdaq added 0.22% and Dow Jones rose 0.20%

Stocks in Asia traded lower. S&P/ASX 200 fell 1.10% and Kospi lost 0.17%. Nikkei and Chinese indices were closed for holidays.

DAX futures point to a lower opening of the European cash session today

Analysts from BNZ, ANZ and Westpac all anticipate 50 bp hike in the Fed funds rate

Beijing authorities closed around 10% of subway stations due to covid-19

Goldman Sachs expects the RBA cash rate at 2.6% by the end of the year

RBNZ Governor Orr says can’t rule out a global recession in the months ahead

Musk considers charging commercial/government Twitter users

China’s independent refiners start buying Russian oil at steep discounts, according to Financial Times

Australian retail sales in March rose to 1.6% (vs. expected 0.6%)

Australian Markit Services PMI for April 56.1 (prior 56.6)

Australian April Construction PMI 55.9 (vs. prior 56.5)

New Zealand unemployment rate in Q1 3.2% (vs. 3.2% expected)

API report showed larger than expected decline of US crude stocks

Oil is trading higher while natural gas fell 1.0%

Precious metals remain under pressure. Gold fell slightly to $1865, while silver trades around $25.55

AUD and CAD are the best performing major currencies while GBP and NZD lag the most

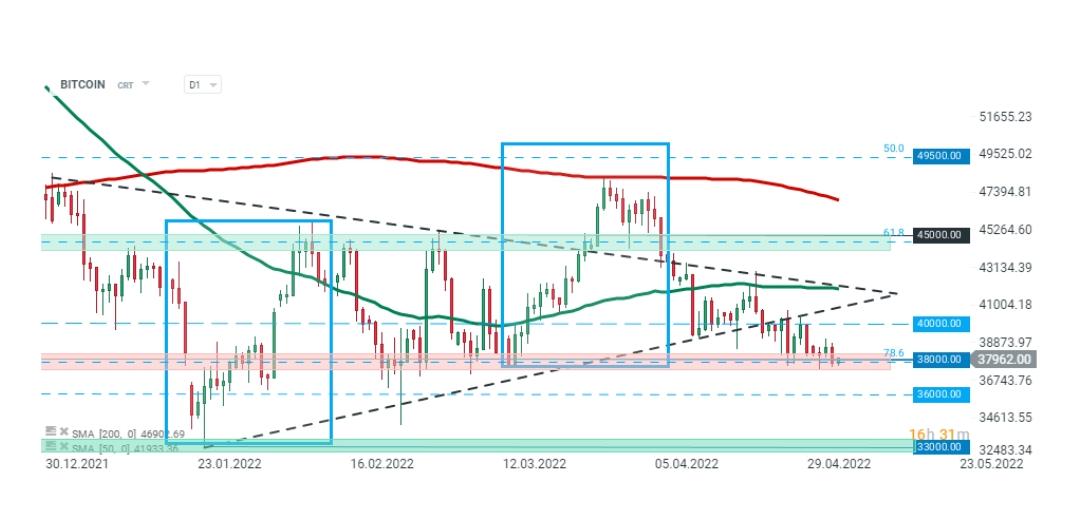

Cryptocurrencies trade higher – Bitcoin gains 0.7% while Ethereum trades 0.6% higher.

Bitcoin continues to test major support around $38,000, which coincides with 78.6% Fibonacci retracement of the upward wave launched in July 2021.

+35726030417

+35726030417 support@Forextk.com

support@Forextk.com Android app

Android app